Google I/O 2026 Was a Consumer Keynote in an Enterprise Year

I watched Google I/O on May 19, 2026. By the end of the keynote, something felt off and I couldn’t say what.

Gemini Spark, the keynote’s headline AI agent, was on a US-only Ultra waitlist starting “next week.” Antigravity 2.0 shipped that morning by forced auto-update, replacing a working IDE with a chat-only Agent Manager and breaking auth on first login for many users. Gemini 3.5 Flash benchmarked roughly 2 to 3 times more expensive per task than the Gemini 3.1 Pro it routed traffic away from. The new Pro was pushed to June. The intelligent eyewear was scheduled for fall, audio version only. Smart glasses with displays had no release date.

It was a consumer keynote.

Then Alphabet reported its Q1 numbers on April 29, 2026. Of the company’s record $62.6 billion Q1 net income, approximately $28.7 billion came from re-marking the equity stake it owns in Anthropic. Nearly half of Alphabet’s record-breaking quarter came from owning a piece of one of the labs Google is publicly competing with. That line on the earnings statement, more than anything Sundar Pichai said on stage at I/O, told me where the AI race had moved in 2026.

The customers paying closest attention to Google’s AI products right now are the most dissatisfied. The Reddit subs that are nominally pro-Gemini are angrier than the ones that have always been skeptical. And at the layer where enterprise AI work actually gets built (skills, plugins, MCP servers, central team management, the connective tissue between people and tools), Google didn’t show up. Anthropic did. I know this because I’m building that kind of system for a client right now, on Anthropic’s stack. Google doesn’t have the equivalent components, and I/O 2026 did not announce them.

What Google Actually Announced

Every headline announcement from I/O 2026 was a consumer-facing product, app, or price-tier reshuffle.

Gemini 3.5 Flash shipped as the new default model across the Gemini app, Search, AI Studio, and Antigravity. There was no Gemini 3.5 Pro at launch; it got pushed to June, with 3.1 Pro still the only Pro option. The knowledge cutoff, set in January 2025, has not moved across four consecutive Gemini model versions (2.5 Pro, 3, 3.1, 3.5). When a paid Gemini AI Pro user hits the new compute cap, they get silently downgraded to Flash-Lite, the smallest model in the family. Pre-I/O an AI Pro subscriber had roughly 33 times the daily quota of a free user. Post-I/O it is 4 times.

Gemini Spark was the keynote centerpiece, a 24/7 personal AI agent running on a Google Cloud virtual machine while your laptop is closed. It is on a waitlist for US Ultra subscribers starting next week. Everyone else: trusted-tester status. Third-party MCP integrations and payment authorization are pushed to summer.

Antigravity 2.0 shipped at the keynote and immediately ran into a wall. The forced auto-update overwrote the IDE with a chat-only “Agent Manager.” Extensions, MCP configs, and projects disappeared because the installer wrote to a different folder than v1 used. Auth failed on first login for many users. The product immediately fragmented into three confusingly-named apps (Antigravity 2.0, Antigravity IDE, Antigravity CLI). Pro users reported burning their weekly cap in 42 to 75 minutes.

The AI Pro and AI Ultra plans were reshuffled the same week. A new $100 AI Ultra tier was inserted. The existing $250 tier was cut to $200. Daily prompt limits were replaced without notice with opaque compute-based 5-hour and weekly caps. AI Studio’s temperature and top_p sliders were removed for the new Flash model.

Intelligent eyewear: audio-only glasses this fall with Gentle Monster, Warby Parker, and Samsung. Display variant: no release date.

Absent from the keynote: Gemini 4, Gemini 3.5 Pro live, a new Veo, a new Nano Banana, new Pixel hardware, Android news.

None of it was at the enterprise connective-tissue layer. None of it was for IT departments standing up cross-team AI infrastructure. A consumer keynote.

The People Paying Attention

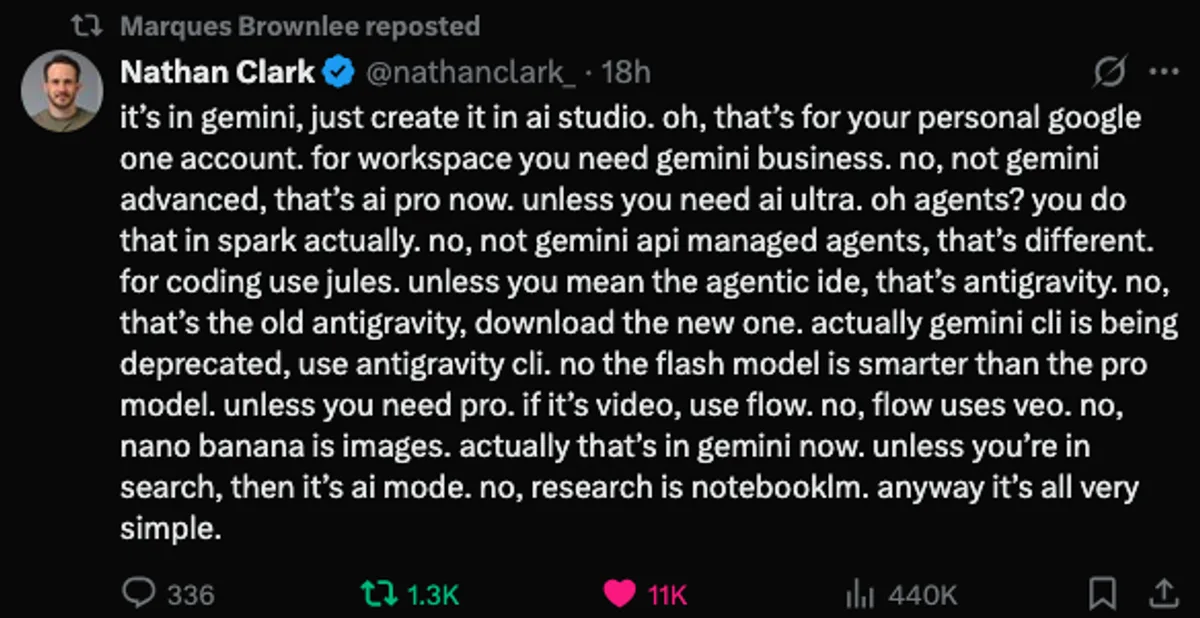

The tweet above, written by Nathan Clark and reposted by Marques Brownlee, hit 11,000 likes and 440,000 views within 18 hours of the keynote. The joke only lands if you know all the products. To understand why it’s funny, you have to be paying close enough attention to Google’s AI lineup to recognize each item being mocked.

Across the same week, the most-loyal Gemini subs went from defending the platform to cancellation announcements. Three things stacked up.

On May 17, two days before the keynote, Google swapped Gemini’s daily prompt counters without notice for opaque compute-based caps: a rolling 5-hour window plus a hard weekly ceiling, with no visible token meter. Users were already being throttled before any announcement. The email explaining the change reached AI Pro subscribers on May 20, three days after the change took effect. One Reddit user on r/Bard reverse-engineered the new caps and worked out that Google gives Pro subscribers roughly $1.50 worth of compute per 5-hour window for $20 a month, and the dashboard doesn’t show what’s being counted.

Two days later, on May 21 in the morning, Google’s Antigravity product head posted a “3x usage forever” announcement intended as a fix. Hours later, that same person posted again, announcing another 3x increase on the weekly cap because users were still hitting walls. Google walked back the walkback within hours of issuing it. The top comment on the second post simply read: “3x but still less then 5.17.”

The third thing was longer in the making. Gemini CLI had launched June 25, 2025 as “your open-source AI agent” with “the industry’s largest free allowance” of 1,000 daily requests. Over eleven months it attracted roughly 100,000 GitHub stars, 13,800 forks, and 6,000 merged community pull requests. On May 19, 2026, Google announced the sunset for June 18, 2026. The transition post does not contain the words “open source.” The replacement, Antigravity CLI, is closed-source, and by Google’s own admission “won’t have 1:1 feature parity right out of the gate.” Eleven months from launch as a community-built open-source agent to a closed-source replacement.

Each of those alone would have created a Reddit rage cycle. Stacking them in the same week, in front of an audience watching for keynote announcements, is why the threads on r/Bard, r/GeminiAI, r/google_antigravity, and r/GoogleAntigravityIDE are full of cancellation posts right now.

Anthropic has done quieter versions of the same. On April 21, 2026, Anthropic stealth-removed Claude Code from the Pro plan, then reverted after backlash. On May 13, an SDK credit cap on the Max plan effectively shrank usage limits by about 10x. OpenAI has run its own series of quiet downgrades through 2025 and 2026. The AI-subsidy era is ending across the board. The companies that handle the transition openly, with notice and grandfather clauses, will keep their trust. Google did it loudest in one week, with everyone watching.

The Layer that Actually Matters

The AI race in 2026 has moved two layers above where most keynotes point. The model layer (which lab has the smartest single model) has converged into a 1-to-2 point benchmark race that changes monthly. The harness layer (which IDE or CLI you use to drive the model) is now five large players plus a long tail. The layer where companies actually build something durable sits above both: skills, plugins, MCP servers, hooks, and the central management primitives that let an organization roll capabilities out to teams under proper permissions.

This is the layer Anthropic has been building since November 2024. I wrote about it at length in How Anthropic Is Quietly Winning the AI Race two months ago. Anthropic added Cowork as the non-developer surface consuming the same plugin format that Claude Code uses. The plugin bundle now packages five primitives together (skills, MCP servers, slash commands, subagents, hooks) in a single git-versionable artifact. The enterprise allowlist primitives (strictKnownMarketplaces, forcedPlugins, hostPattern) shipped to production. Plugin marketplaces can be hosted privately and pinned by git ref, with MDM-compatible deployment for IT teams using Jamf or Ansible.

Compare that to Google’s position at the same layer.

Google officially adopted MCP on December 11, 2025. That was 13 months after Anthropic shipped MCP, and several months after OpenAI, Microsoft, and most of the relevant ecosystem had already standardized on it. Google’s own competing protocol, Agent2Agent (A2A), was donated to the Linux Foundation in June 2025 after failing to gain traction at the agent-to-tool layer. As of May 2026, analysts position A2A as complementary to MCP rather than competitive. The standard for cross-agent and cross-tool communication was built by Anthropic and adopted by Google over a year later.

Google’s flagship “agentic” projects from the past two years are all still in trusted-tester status 17 to 24 months after their first public demo. Project Astra (announced May 2024). Project Mariner (December 2024). Project Jules (December 2024). Jules did not appear at I/O 2026 at all. Its PM later said: “We weren’t at I/O because we weren’t ready for it, truthfully.”

The customer scale stories make the gap concrete.

Anthropic’s headline enterprise wins are workforce-wide deployments using Claude + MCP + Agent SDK as a shared substrate. Cognizant committed 350,000 employees. Deloitte committed 470,000 employees. Hitachi committed 290,000 employees. Block deployed across 12,000 employees and 15 job functions. The same plugin format and the same connectors across teams that don’t normally share much.

Google’s comparable enterprise wins are agent-count stories inside a single organization. GE Appliances deployed roughly 800 agents across its Brilliant Factory operations. KPMG reported 100+ internal agents in the first month. Tata Steel has roughly 300+ agents across nine months.

Both kinds of deployment exist. They are different shapes of scale. Anthropic’s win shape is “one shared brain across the entire workforce.” Google’s win shape is “many specialized bots inside one operation.” For companies trying to build the cross-team connective tissue I described in When Every Team Shares One Brain, the first shape is what you need.

At the IDE layer specifically, Cursor 2.5 matched Anthropic’s five-primitive plugin bundle in February 2026, with its own marketplace and team-distribution modes shipped on May 1. Cursor is IDE-only though, has no equivalent to Cowork for non-developers, and its current push toward more autonomous agents (Cursor 3 in April, Composer 2.5 on May 18) is alienating the IDE-first developer base it grew with. Cursor matters at the IDE layer. It doesn’t run the kind of company-wide deployment this article is about.

From the Trenches

I picked up Gemini CLI the day it shipped in June 2025. I wanted it to work. I’d been using Claude Code in parallel, and the question was whether Google’s open-source agent would catch up.

It didn’t. Hooks landed in Claude Code first. So did skills, the marketplace, and the plugin format that bundles skills, MCP servers, commands, subagents, and hooks into one git-versionable artifact. Each of those primitives is what you actually compose with when you build a serious deployment. Gemini CLI never reached that level. Codex CLI from OpenAI still hasn’t either. By March of this year I’d moved my own work entirely. The deciding factor was the ecosystem layer. Model quality among the top three labs by mid-2026 is effectively a wash.

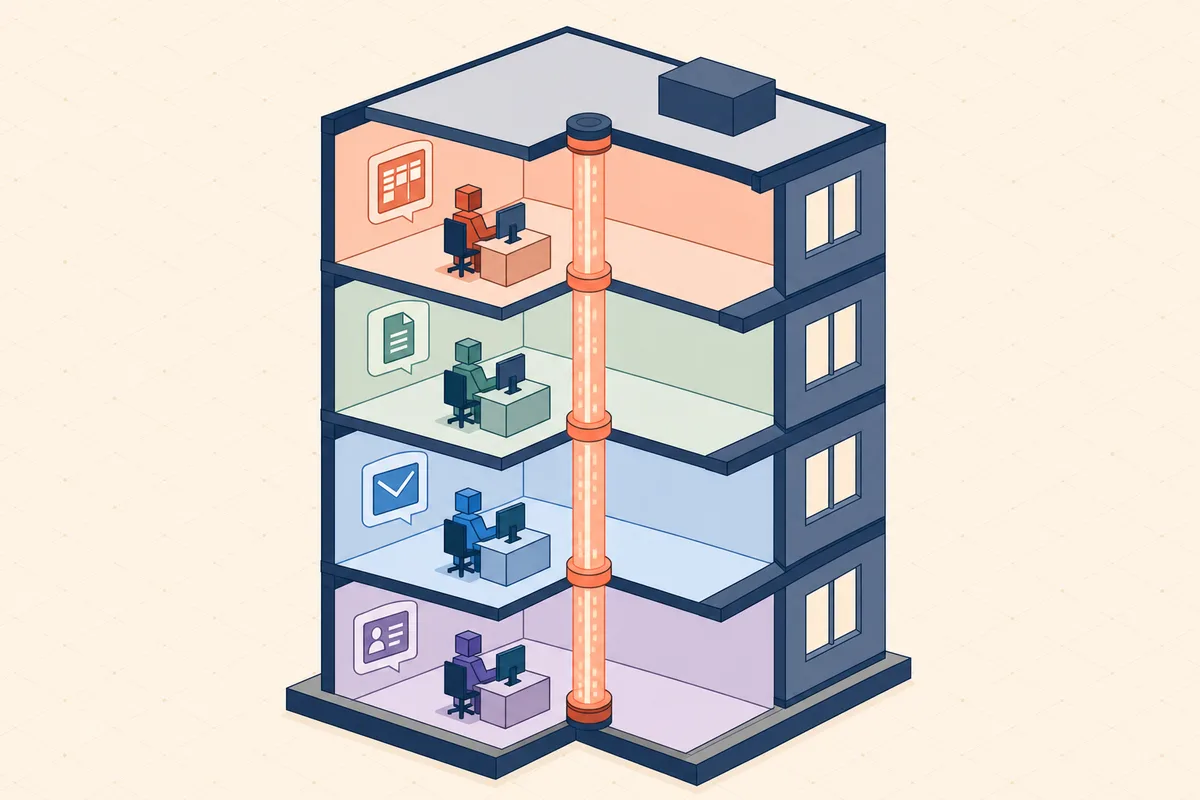

Right now I’m deploying that ecosystem layer at a client. The setup, in concrete terms: Jira, Notion, Gmail, web search, Apollo, and Lemlist are connected to Claude via MCP. Custom skills and plugins are distributed through an internal marketplace. Each team has its own permission scope. Salespeople can’t reach engineering’s source code, engineering can’t see finance’s reports, nobody outside HR can query employee records. Least-privilege, applied per team. Inside each scope, individual users have token budgets. Management has fine-grained monitoring on what’s being accessed and what’s being generated.

The cross-functional information flow I described in Becoming a Company Where Every Team Shares One Brain is running in production at a client right now. A salesperson preparing for a client meeting can ask the system to produce a pre-call brief. The brief automatically includes warnings like: “avoid demoing discount stacking during this call; BILL-2847 is in progress, not yet shipped.” The known-bug context came from engineering’s Jira. Customer history from Gmail. Deal stage from Apollo. Competitive notes from Notion. No human had to forward anything. The brief reflects the company knowing what the company knows.

Sharp edges, since the article is more useful with them in it.

Observability was rough for the first month. The default Cowork telemetry didn’t surface the right signals for the kind of cross-team access policies we wanted to monitor. Anthropic shipped meaningful improvements within a couple of weeks and the gap closed. But it was a real gap.

Connector coverage is real but incomplete. The standard MCP servers handle the obvious tools well. If a team uses an internal system, or a niche vertical SaaS, or any tool without a public MCP server, somebody technical has to build it. Most companies stall at exactly this point. They get the Cowork deployment partway there, hit a missing primitive, and don’t have the in-house engineering capacity to fill the gap.

This is the work I do. I handle the assessment, the MCP server engineering, the skill and plugin authoring, and the team-level rollout that gets a deployment past the “almost there” point. I should be transparent that this is exactly the work being described above. I have skin in this game.

Maybe It’s on Purpose

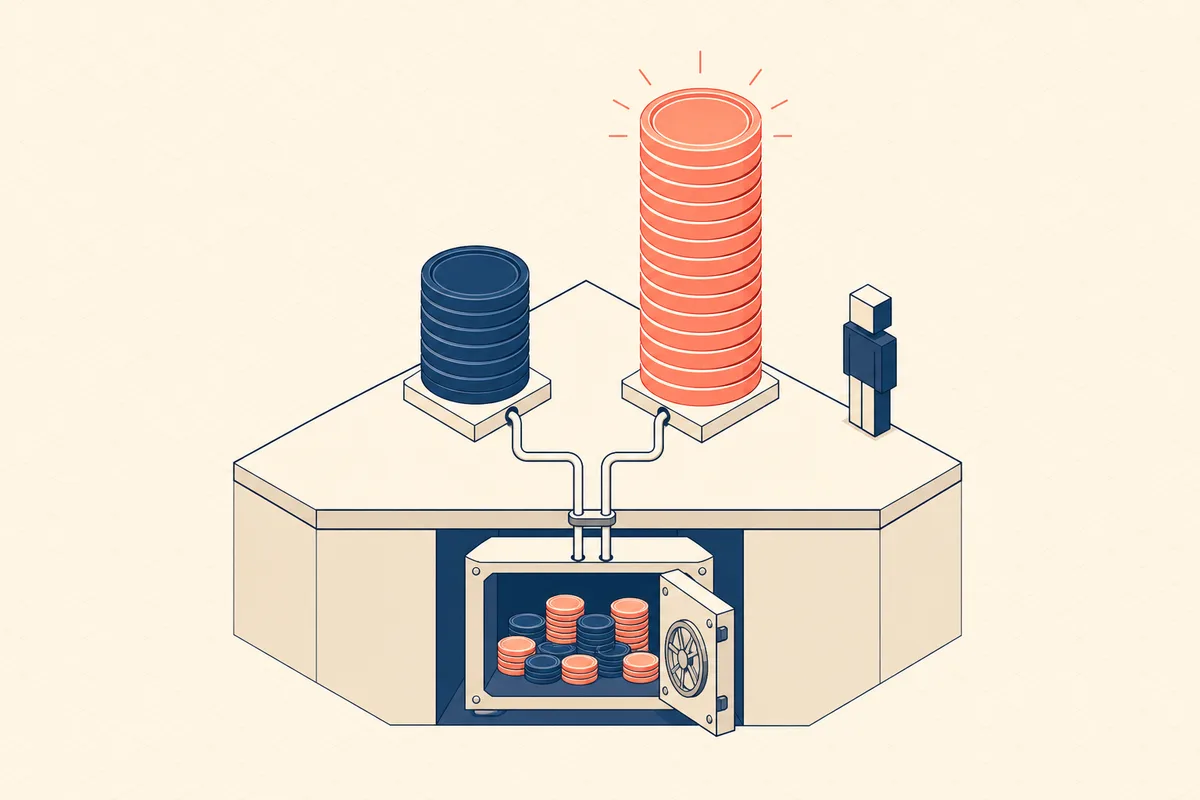

Alphabet’s Q1 2026 record-quarter profit was $62.6 billion. Of that, approximately $28.7 billion came from mark-to-market gains on the equity stake Alphabet holds in Anthropic. As Fortune ran the numbers on April 30, 2026: “Nearly half of Alphabet’s record $62.6 billion profit did not come from search ads, cloud services, or any of its products at all. It came from Alphabet updating the value of the equity it owns in private companies, primarily Anthropic.” Alphabet earned more from owning a piece of Anthropic in Q1 than from any of its own products.

The compute side of the balance sheet is just as structural. Anthropic reportedly committed approximately $200 billion in Google Cloud spending across five years. Anthropic accounts for more than 40% of Google Cloud’s $460 billion-plus backlog. The hardware commitment is up to 1 million TPUv7 chips. Whether Claude leads the model layer, Gemini leads the model layer, or they trade leads over the next decade, the spend hits Google Cloud’s revenue line.

Thomas Kurian, the CEO of Google Cloud, was unusually direct about it on Stratechery in April 2026. Google, he said, doesn’t “see it as a zero sum” with Anthropic. As a platform player, “we have to allow our technology to be monetized in as many ways as possible,” and “most of the large AI labs use our stack.” That is unusually explicit language for a public competitor to use about a frontier model rival. Google is consciously playing a platform-monetization game.

Wall Street has been pricing accordingly. Mizuho raised Alphabet’s price target to $460 in April 2026 on a thesis that explicitly modeled 70% Google Cloud revenue growth through 2026. Loop Capital raised its target from $355 to $490. Bernstein reframed the AI market in May 2026 as “a two-vendor market on the lab side, three-vendor market on the cloud side.” The drivers cited in all three raise notes are Google Cloud infrastructure revenue and Anthropic’s mark-to-market. Gemini leadership doesn’t appear.

Whether or not Google planned it this way, the financial structure is unambiguous: Alphabet now profits more from owning a slice of Anthropic than from competing with it. Sundar Pichai and Thomas Kurian are still publicly contesting the enterprise model layer. That posture is real. The mark-to-market on Anthropic is also real, and it is bigger. Nobody at Google has to admit it. The income statement says it.

Where This Leaves Us

Google I/O 2026 was a consumer keynote in a year when the enterprise AI work moved to the connective-tissue layer. The customers paying closest attention to Google’s AI products spent the week of I/O documenting how they felt rugpulled by silent plan changes, force-updates, and an open-source sunset. The layer where companies build durable infrastructure was not announced on stage, because Google hasn’t built it.

Two months ago I wrote that Anthropic was quietly winning the AI race. As of March 2026, Anthropic’s ARR was $19 billion. As of April 2026, The Information reported it had passed $30 billion. The growth rate hasn’t slowed. Two months later the picture is sharper.

If you run an organization in 2026, the layer actually doing the work is the connective tissue between teams, tools, and people: the skills, plugins, MCP servers, and central management primitives that let a company build a shared brain. Anthropic has shipped that as a coherent stack. Google announced consumer products instead.

This is a snapshot taken in May 2026. The verdict isn’t in yet. Spark could become a real product. Antigravity 2.0 could stabilize. Google’s TPU moat is real. Anthropic’s own pricing rugpulls are real.

Most consumers still think of the AI race as ChatGPT vs Gemini. The companies actually building infrastructure that will matter in 2027 have already moved one layer up. Google I/O 2026 showed which lab has built at that layer, and which hasn’t.